Once invested in a startup that is EIS or SEIS eligible, they can receive income tax relief. However, few individuals know how to claim EIS and SEIS tax relief in practice.

In this blog post, I will explain to you what is EIS and SEIS, the rules you should be aware of when claiming your SEIS and EIS tax relief and how to claim your SEIS and EIS tax relief.

What are the EIS and SEIS?

EIS and SEIS have always served the same essential purpose: to channel early-stage investments into high growth potentials.

However, although SEIS and EIS are very similar in many aspects, there are some differences you need to know.

The main difference is that there are different criteria for startups seeking to be part of either EIS or SEIS.

More extensive and older companies use EIS (although, in the sense of the market and corporate environment in the UK, they are still considered small and young). Meanwhile, SEIS primarily aim at startups and very early-stage businesses.

To be eligible, a company must:

- Trade under the SEIS must be less than 2 years or 7 years under the EIS

- Have less than 25 employees under SEIS or 250 for EIS

- Have no more than £ 200,000 or £15 million of gross assets for EIS

Similarities between SEIS and EIS include the absence of having to pay any inheritance tax on shares kept for at least two years. You can even offset the loss from their tax on capital gains if the shares are sold at a loss.

What is SEIS Tax Relief?

The SEIS (Seed Enterprise Investment Scheme) was launched by HM Revenue & Customs (HMRC) in April 2012. The United Kingdom government developed it to help small, early-stage companies raise funds by offering tax relief on investments made into qualifying companies through individual investors.

SEIS offers some of the world’s best tax reliefs. SEIS allows up to 50% of your investment to be claimed back in income tax relief and provides substantial tax reductions on capital gains.

For startups at an early stage, SEIS lets you raise the capital you need to expand by providing substantial tax relief to investors in your business, making a potential investment in your company more attractive.

SEIS allows early-stage companies to invest up to £100,000 per tax year and receive a tax break of 50% in return.

If you invest in SEIS, you can also benefit from a tax exemption on capital gains on any revenues resulting from selling the shares after three years. You also have no inheritance tax to pay on your SEIS shares held for at least two years.

Additionally, if your shares are sold at a loss, you may offset the loss against their capital gains tax.

SEIS Tax Relief Examples

An example of SEIS Tax Relief can be found in these three scenarios:

Assuming an Income Tax rate of 45% and you owe Capital Gains at 28%, you invest £3, 000 and receive £1, 500 in Income Tax Relief.

If the company you’ve invested in fails, your shares are worth £0, but you receive £675 loss relief (50% investment x your tax rate).

When the company breaks even, you sell your shares for £3, 000 after three years, having already claimed £1, 500 in Income Tax relief. You get £4, 500 back.

If the company doubles in value, your shares are worth £6,000. You don’t have to pay Capital Gains Tax on the profits from shares you’ve held for more than three years.

What rules should you be aware of when claiming your EIS and SEIS tax relief?

In claiming your tax relief, there are specific rules that you should be aware of. These include:

Share “Termination Date”

To benefit from income tax exemption, SEIS or EIS shares must be kept for a minimum of three years and, as such, should be considered as a long-term investment.

The date on which you must retain your claim before the share termination date on your S/ EIS certificate is shown. You will have to inform HMRC and repay any income tax relief you have claimed if the shares you’ve held for 3 years are sold.

Investor tax reference

Not all investors will have an Investor Tax Reference Number, so include your National Insurance Number instead of allowing HMRC to link your claim for tax relief.

Tax relief for a different year

HMRC outlines a chance to back-date the tax relief claim to previous tax years. A ‘carry back’ facility makes it possible to classify all or part of the expense of shares purchased in one tax year as if those were acquired in the previous tax year.

Instead of the tax year in which such shares were purchased, relief is provided against the previous year’s income tax liability. This is subject to the overriding limit for relief for each year.

SEIS Claim Requirements

You will generally claim EIS tax relief when you complete your tax return. Any data that is included in your EIS3 certificates will be requested.

These are the certificates you receive from each company you invested in, typically a few months after the investment. If you invested in a fund, you would typically receive one EIS3 for each underlying company.

These are certificates you usually receive a few months after the investment from each company you invested in. You will normally receive one EIS3 if you invest in a fund for each underlying company.

The fund manager will give you a single EIS5 certificate in the rare event you have invested in a ‘Registered EIS fund.

Both EIS3 certificates and EIS5 certificates contain the same details you need:

- The name of the company that you have invested in

- The amount you subscribed to and which can be claimed for tax relief

- The date on which the shares were issued (usually different from the date on which you invested)

- Name of relevant HMRC office and its reference

What you decide to do next depends on how you plan to submit your tax return (post or online). There is also an alternate method to use in some instances, such as whether you do not want to claim tax relief for the same tax year for which you are filing a return or don’t habitually file a tax return.

How to claim SEIS tax relief

Option 1: On your Paper Tax Return

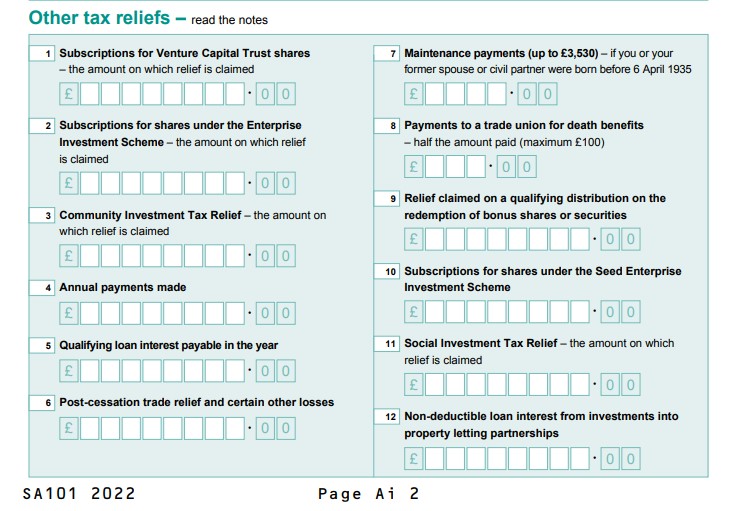

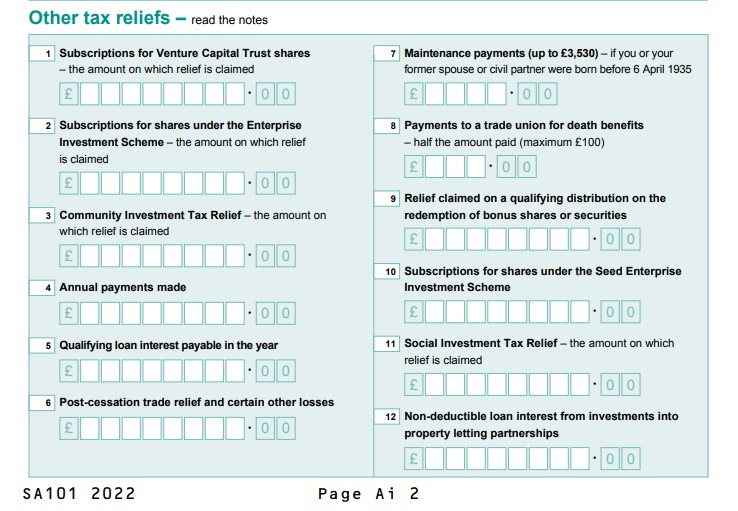

- The “Additional Details” sheet (Form Sa101) will need to be completed and included with your return.

- In box 10 (Subscriptions for shares under the Seed Enterprise Investment Scheme) of the “Other tax reliefs” section, on the page, Ai 2, write the total amount of all your SEIS subscriptions on which you wish to claim tax relief.

Note that for the investments you are claiming tax relief, HMRC does not ask you to send SEIS3 certificates. However, they might ask you about it, so ensure you keep them safe.

The tax you must pay will be reduced by tax relief claimed by your tax return. If you’ve already paid too much income tax, the excess can either be repaid by cheque or directly into your bank account.

Option 2: On your Online Self-assessment

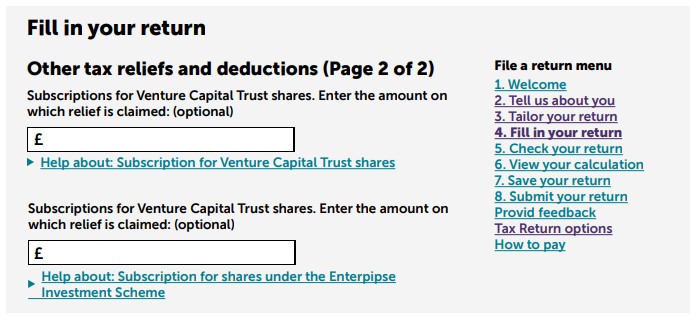

- Answer “Yes” to the question in section 3 on other tax reliefs “Tailor your return”.

- In the section ‘Other tax relief and deductions (Page 2)’ of section 4, ‘Fill in your return’, enter the total sum of all your SEIS subscriptions on which you want to receive tax relief and include information on each of your SEIS investments.

Again, take note that for the investments on which you are claiming tax relief, HMRC does not ask you to send SEIS3 certificates. However, they might ask you about it so make sure that you keep them safe.

The amount of tax you need to pay will be reduced by tax relief claimed by your tax return. If so much income tax has already been paid, the excess can either be returned by cheque or directly into your bank account.

Option 3: Fill out the SEIS3 Form

There is also an alternative form of claiming SEIS tax relief. The claim form you receive (on pages 3 and 4 of SEIS3) can be completed and sent to your HMRC tax office.

There are some conditions that you can use this method. These include:

- If you want to claim your tax relief against the previous year. This could be the case if you want to use ‘carry back’ or if you have not obtained your SEIS3 certificate in time for the tax return deadline.

- If you pay tax via PAYE and choose to claim the tax credit by changing your tax code and investing in SEIS, and receiving your SEIS3 certificate early in the tax year, this could be an option. When you file your tax return, you also need to enter the details of the claim.

- If you want to claim income tax relief as well as capital gains reinvestment relief.

You could also use this method if you don’t habitually file a tax return, such as if all of your tax is paid at source through PAYE. If you have other questions, you can consult HMRC’s full guidance on the subject.

What do you need on hand to claim EIS tax relief?

You will usually claim EIS tax relief when you complete your tax return. Some information included in your EIS3 certificates will be requested. These are certificates you earn, usually a few months after the investment, from each of the firms you invested in.

If you have invested in a fund, you will usually receive one EIS3 for each of the underlying companies. In the rare occurrence, you invested in an “Approved EIS fund,” the fund manager will send you a single EIS5 certificate.

Both EIS3 certificates and EIS5 certificates contain the same details you need:

- The name of the company that you have invested in

- The amount you subscribed to and which can be claimed for tax relief

- The date on which the shares were issued (usually different from the date on which you invested)

- Name of relevant HMRC office and its reference

How to claim EIS tax relief

Option 1: On your Paper Tax Return

- The “Additional Details” sheet (Form Sa101) will need to be completed and included with your return.

- Write the total amount of all your EIS subscriptions on which you wish to claim tax relief in box 2 (“Subscriptions for shares under the Enterprise Investment Scheme”) of the “Other tax reliefs” section, on page Ai 2.

Note that HMRC does not ask you to send EIS3 or EIS5 certificates for the investments you are claiming tax relief. However, they might ask you about it so make sure that you keep them safe.

The amount of tax you need to pay will be reduced by tax relief claimed by your tax return. If so much income tax has already been paid, the excess can either be returned by cheque or directly into your bank account.

Option 2: On your Online Self-assessment

- You must respond “Yes” to the other tax relief question in section 3, “Tailor your return.”

- You have to enter the total sum of all your EIS subscriptions on which you want to claim tax relief in the section’ Other tax relief and deductions (Page 2)’ of section 4, ‘Fill in your return’ and may include information of each of your EIS investments.

Again, note that HMRC does not ask you to send EIS3 or EIS5 certificates for the investments for you are claiming tax relief. However, they might ask you about it, so make sure that you keep them safe.

The amount of tax you need to pay will be reduced by tax relief claimed by your tax return. If so much income tax has already been paid, the excess can either be returned by cheque or directly into your bank account.

Option 3: Fill out the EIS3 Form

There are some conditions that you can use this method. These includes:

If you want to claim your tax relief against the previous year. This may be the case if you want to use ‘carry back’ or if you have not obtained your SEIS3 certificate in time for the tax return deadline.

- If you pay tax via PAYE and choose to claim the tax credit by changing your tax code and investing in SEIS, and receiving your SEIS3 certificate early in the tax year, this could be an option. When you file your tax return, you also have to enter the details of the claim.

- If you want to claim your deferral relief as well as income tax relief.

You could also use this method if you don’t habitually file a tax return, such as if all of your tax is paid at source through PAYE. If you have other questions, you can consult HMRC’s full guidance on the subject.

Summary

There are different ways how you can claim your SEIS and EIS tax relief. If you are interested in investing in SEIS and EIS, you can start reading this guide or you can schedule an appointment with us today.

Rest assured that someone will get in touch with you and help you every step of the way.